The SER and the Dutch Accounting Standards Board (Raad voor de Jaarverslaggeving) have compiled the frequently asked questions and answers below based on thousands of questions from companies and organisations preparing for the Corporate Sustainability Reporting Directive (CSRD). These questions are also bundled in the question-and-answer documents that you can find here. Do you have other questions about the CSRD, ESRS (European Sustainability Reporting Standards) or are you missing a question in this list? Look at the bottom of this page.

These questions and answers were last updated on 5 March 2026. For the latest updates since that date, please see the bottom of this page.

Introduction CSRD

What is sustainability reporting?

In a sustainability report, the undertaking provides insight into its strategy and policy on sustainability. The report also contains information on how the undertaking implements these and what the effects are. Sustainability is a broad concept that is often connected to ESG, which stands for Environment (E), Social (S) and Governance (G).

What is the CSRD?

The CSRD (Corporate Sustainability Reporting Directive) is a European Directive that requires certain undertakings to report on sustainability in a sustainability report. This sustainability report is part of the management report. The sustainability report must be reviewed by an external auditor. The CSRD describes what information the sustainability report must contain. The undertaking should address in the report:

the undertaking's impact on people and the environment.

the role of sustainability in the governance of the undertaking.

the financial sustainability risks and opportunities of the undertaking for the short (1 year), medium (5 years) and long term (>5 years). The undertaking pays attention to both actual and potential future impacts, risks and opportunities.

how sustainability is part of the business strategy, policies and risk management processes, and what the undertaking aims to achieve in terms of sustainability.

The first undertakings report in line with the CSRD as of the 2024 financial year.

More information:

Reference is made to questions under 'Scope - to whom does the CSRD apply?'.

Who created the CSRD and what is its status?

The Corporate Sustainability Reporting Directive (CSRD) is a European Directive originating from the European legislator. The CSRD was published in the Official Journal in December 2022 and entered into force on 5 January 2023. From that moment, national legislators from EU Member States, such as the Dutch legislator, had 18 months (until July 2024) to transpose the CSRD into national law (implementation period). The Netherlands has not met the implementation deadline. It is not yet clear when the CSRD will be transposed into Dutch law.

At the beginning of 2026, the CSRD was simplified as a result of the Omnibus proposals of the European Commission. These changes must also be implemented in national law.

The European Commission formulated three goals for sustainability reporting requirements. It is important to keep these in mind when reporting on the CSRD requirements:

reduce systemic risks related to climate change and other sustainability topics such as human rights;

change capital flows, and ensure that more investments are made in sustainable activities, and less in unsustainable activities;

taking responsibility for issues relating to their impacts on society and the environment.

How does CSRD fits into the broader ESG landscape?

In the Paris Agreement, it has been agreed to limit global warming to a maximum of 2 degrees Celsius. A number of measures and policy initiatives, including the "Green Deal", should help the European Union to move towards an economy that is climate neutral by 2050, grows without resource depletion and in which no person or region is left behind.

In order to finance the green transition, public and private funds need be channelled to sustainable economic activities. This requires insight into the sustainability of undertakings so that investors or banks can make choices in where they invest, or to whom they grant loans and under what conditions. The CSRD contains the legal obligation to prepare and publish a sustainability report. That report contributes to insight in how sustainable an undertaking is and provides the foundation for a conversation with its stakeholders on this. The CSRD is not limited only to environmental matters, but explicitly also includes all other aspects of ESG. An integral approach of these three ESG topics (environment, social and governance) is necessary to make a positive impact on society and the environment.

Can the implementation of the CSRD lead to different requirements requirements between EU member states?

A European Directive, such as the CSRD, must be implemented as accurately as possible in the laws of the Member States. In this way, laws are comparable. A Directive can contain choices. These are referred to as Member State options, where the EU Member States have the freedom to make choices within the framework provided by the Directive. These options may therefore lead to differences between Member States.

The CSRD also contains several Member State options. Examples include, in short, allowing that:

information may be omitted if its disclosure would jeopardise the commercial position of the undertaking;

the assurance of the sustainability reporting may be conducted by a different entity than the one who carries out the financial audit;

an independent assurance provider may assure the sustainability reporting.

In the explanatory notes to the proposed Dutch implementation decree on sustainability reporting, the Dutch legislator indicates that it intends to implement the CSRD without adding national requirements (“gold-plating”). The option to allow an accredited independent assurance services provider to assess sustainability reporting is not adopted. Further research is required before this option can be incorporated into Dutch law.

You can find an overview of member states' national implementation legislation on Eurlex, a website on European law run by the Publications Office of the European Union. Commercial parties also track implementation in the various member states, see for example the ‘CSRD Transposition Tracker’, created by a collaboration of international law firms.

More information:

The most recent version of this CSRD Transposition Tracker can be found on the Ropes & Gray website. Ropes & Gray and its collaboration partners are not affiliated with the SER nor the DASB and have not been involved in the development of this document.

How will the CSRD be implemented in Dutch law?

The implementation of the CSRD into Dutch legislation has not yet been completed. The intention is that the implementation will take place through a decree and a legislative act that will enter into force at the same time:

Implementation Decree on sustainability reporting

This general administrative order contains the actual obligation for legal entities to include a sustainability report in the management report.

Legislative Act implementing the sustainability reporting directive

This legislative act contains the elements of the CSRD that are not included in the Implementation Decree, such as the mandatory assurance of sustainability reporting and the method of publication of sustainability reporting as part of the management report.

What are the key changes to the management report by the CSRD and ESRS?

The following list contains some significant changes to the management report by the CSRD and ESRS:

the management report is extended with a sustainability report;

the sustainability report becomes a separate part of the management report, making it easy to find;

the sustainability report focuses on three main themes: Environment, Social and Governance;

detailed sustainability reporting standards, the ESRS, prescribe how to report;

double materiality is the starting point. The undertaking reports on the impact of sustainability factors on the undertaking and on the impact of the undertaking on the value chain, people, environment and animals. The reporting addresses actual and potential impacts, and covers short-, medium- and long-term;

the sustainability report is assessed by an external auditor;

the sustainability report must be submitted in a digital format to the Chamber of Commerce and must be made publicly available.

What are the reasons to publish a sustainability report?

There are several reasons why an undertaking should publish a sustainability report in accordance with the CSRD and ESRS or VSME. Possible reasons are:

the legal obligation to publish in line with CSRD and ESRS. Undertakings that are in scope of the CSRD are required to publish a sustainability report.

anticipate legislation and future legal obligations for reporting in line with the CSRD and ESRS. It takes time and resources to report according to the CSRD and ESRS, so it is important to be proactive and being preparing already;

create trust with the financial markets and improve access to capital;

anticipate (future) requirements for information from customer and clients who fall under the CSRD / ESRS and proactively provide information toward them;

competitive advantage – undertakings that are transparent on their sustainability performance can maximize their competitive advantage;

protect the undertakings reputation, build brand value, and improve trust with consumers;

cooperation across the value chain to make impact. Value chain improvements are easier when there is transparency across them, for example, because they themselves can see overlap on themes or production sites;

take responsibility for sustainability performance. This transparency is relevant for a wide range of stakeholders, such as employees, unions, NGOs and value chain partners.

For whom is the sustainability report intended?

The sustainability report is intended for a broad group of stakeholders, as it provides insight into the sustainability impacts, risks and opportunities of the undertaking on its environment and of the environment on the undertaking. Stakeholders can use the information in the sustainability report to gain insight into the undertaking.

The information in the sustainability report provides insight into the financial impact of the environment on the undertaking. This information is relevant for financial stakeholders such as shareholders, banks and creditors.

The sustainability report also contains information on the impact that the undertaking has on its environment. This information is relevant for stakeholders such as employees, trade unions, social partners, customers, local residents, societal organisations and NGOs.

Finally, the information in the sustainability report may also be relevant for stakeholders such as (potential) business partners, governments, analysts and academics.

Double materiality

What is ‘double materiality’?

With a materiality analysis, the undertaking determines which information is relevant to share with its stakeholders. Information is material if its omission, or misrepresentation, could influence the judgement of the user of the sustainability information. Which information is material to an undertaking therefore varies from undertaking to undertaking.

Double materiality entails looking at the undertaking from two perspectives:

the impact on the undertaking (financial materiality); and

the impact of the undertaking (impact materiality).

This is the starting point of the sustainability report.

Double materiality

By means of sustainability reporting, the undertaking provides, on the one hand, insight into how the undertaking is affected by the developments in the field of sustainability, for example the influence of climate change on the business model. This is called financial materiality.

On the other hand, the undertaking reports on what kind of influence it has on its environment. Consider, for example, the effect of emissions from production processes on the air quality of local residents. This is called impact materiality.

These two perspectives (the impact on and the impact of the undertaking) together are called 'double materiality'. The sustainability report covers all material information, meaning the information on the topics that is or are material from one or both perspectives.

When assessing materiality, undertakings should consider actual and potential impacts, risks and opportunities as well as negative and positive impacts, risks and opportunities. This should be considered over the short-, medium- and long-term.

All undertakings must report on certain reporting requirements and data points. These are the requirements and data points from ESRS 2 and the thematic ESRS (on the description of processes to identify and analyse material pollution impacts, risks and opportunities). This information is always mandatory, as it is considered material information.

How to prioritize in a double materiality analysis?

All material topics need to be included in the sustainability report. Financial materiality and impact materiality complement each another. Therefore, the sustainability report should include topics that are (1) only material from a financial perspective, (2) only material from an impact perspective, and (3) material from both a financial and material perspective.

Which stakeholders should be involved in a materiality analysis?

Stakeholders play a crucial role in the materiality analysis. Stakeholders are direct or indirect interested parties of the undertaking. The CSRD-ESRS identify two main groups of stakeholders:

Affected stakeholders

Individuals or groups whose interests – positively or negatively – may be affected by the activities of the undertaking and its direct and indirect business relationships within its value chain. Examples include own employees and employees in the value chain, suppliers, customers, consumers, end-users, local communities, persons in vulnerable situations and public institutions. Also included are representatives of affected stakeholders, such as workers’ organisations, trade unions and other experts.

Users of sustainability reports

Primary users of financial statements (existing and potential investors, lenders and other creditors, such as asset managers, credit institutions and insurance undertakings), and other users of sustainability reports such as business partners of the undertaking, trade unions and social partners, civil society and non-governmental organisations, governments, analysts and academics.

Involving affected stakeholders is crucial for the ongoing IRBC due diligence process of the undertaking and the sustainability materiality analysis.

The SER has developed various tools to support undertakings in conducting meaningful stakeholder dialogue, also in the context of the CSRD.

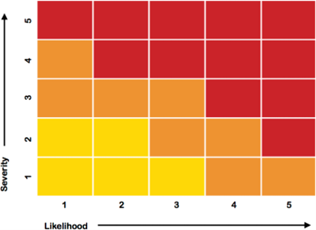

How to determine negative impact materiality?

The ESRS uses ‘impacts’ for both positive and negative sustainability effects of an undertaking, including current and possible future effects. Impact materiality is usually the beginning of the analysis, whereby you can start with negative impacts.

To determine negative impact materiality, you should consider:

the likelihood of a risk occurring and

the severity of the negative impact.

Severity is assessed based on scale, scope and irremediability:

scale refers to the gravity or seriousness of the potential or actual negative impact;

scope refers to the reach or extent of the potential or actual negative impact, for example the number of individuals that are or will be affected;

irremediable character refers to the irreversible nature of the negative impact by looking at the limits on the ability to restore the individuals or environment affected to a situation equivalent to their situation before the negative impact.

Subsequently, you set likelihood against severity and see which negative impacts are material in any case (red) and potentially material (orange), depending on the specific organisation. Severity takes precedence over likelihood. For more information, reference is made to EFRAG's implementation guideline on double materiality.

How to report on financially material ESG topics which are also discussed in the annual financial statements?

This depends on the situation. A sustainability topic that is “financially” material is often, but not always, disclosed in the annual financial statements and could also be part of the corporate report (especially in integrated reporting structures).

An example regarding this has been discussed in the webinar series by the SER and DASB, and relates to the risk of flooding. That is a topic that is relevant for the sustainability report from the financial materiality perspective. However, in the annual financial statements of an undertaking, the direct impact of this risk will only be disclosed after the flood has actually occurred. It is usually not allowed to include forward looking statements such as this within the annual financial statements (in the form of a provision for potential damages).

What sources can I use to determine my social material themes within my own organisation?

To determine the materiality of social issues affecting your organisation or your value chain, you can look, among others, at the following sources:

Employee satisfaction survey (MTO/MO): Survey the satisfaction of your own employees or check if value chain partners are doing this and thus identify sustainability themes around employees that are important for your undertaking.

Safety, health, environment and quality information (SHEQ/KAM): This information can provide insight into relevant topics. See also, for example, the SER OSH Platform for useful tools and information.

Company Emergency Response / Accident registration: Analyse incidents and accidents to identify trends.

Collective bargaining agreement (CLA): Refer to the collective labour agreement for specific agreements and obligations related to working conditions.

Works Council (WC): engage in regular discussions with the WC and gain an understanding of the WC's concerns and the perspective the context of sustainability

Exit interviews: Collect feedback from departing employees to identify potential problems or opportunities.

Conversations on social and psychological safety, diversity and inclusion: Listen to employees to gain insight in certain trends and developments.

Identify vulnerable workers: Consider colleagues on temporary contracts, hired staff (such as security and cleaners), trainees and people with disabilities. Conduct interviews to understand their experiences.

Grievance mechanisms: Analyse the root causes of the grievances that have been received via the grievance procedure. These can give insight in the impact of the organisation on people.

Confidential counsellors within an organization: Despite not being allowed to share information on individual cases, they do have insight into the themes that are material within an organisation around employees.

Review KPIs where available on sickness rate, training, male-female ratio at the top and further in the organisation, turnover, pay ratio. These items are also in the ESRS. For example, if gender (dis)equality emerges as a material issue, the ESRS will help you report on it.

These resources are not exhaustive or mandatory, but can provide a good starting point.

Can you include social contributions from (employees of) the undertaking such as volunteering or supporting social internships in the sustainability report?

Undertakings can include social contributions, such as volunteering or supporting social internships, in their sustainability report if they are material to the undertaking. This demonstrates their positive impact. The ESRS S1 standard provides leaves room for this and show, for example, that it helps own staff to broaden their horizons and develop themselves. These themes can also be part of ESRS S3 ‘affected communities’ and show, for example, how the undertaking is giving something back to communities that may be disadvantaged socio-economically. More information can be found, for example, on the platform Good Busy (in Dutch only).

More information:

Good Busy is an initiative of the Association of Dutch Volunteer Work Organizations (NOV) and is made possible by the Ministry of Health, Welfare and Sport. The program focusses on knowledge and its agenda-setting role on the theme of employee volunteerism.

Amendments to the CSRD through the Omnibus proposals

What are the Omnibus proposals?

The Omnibus proposals are proposals for the simplification of European sustainability legislation published by the European Commission on 26 February 2025. The Omnibus proposals include proposals to simplify, among others, the CSRD, the Corporate Sustainability Due Diligence Directive (CSDDD) and the EU Taxonomy.

On 29 January 2025, the European Commission published the Competitiveness Compass. In this Compass, the Commission outlines, among other things, five enablers for competitiveness. One of these enablers is ‘simplification’. The European Commission published the Omnibus proposals to simplify legislation and regulation in order to reduce regulatory pressure and administrative burdens for undertakings and to strengthen competitiveness.

What is the status of the Omnibus proposals?

The Omnibus proposals include proposals to simplify various European sustainability laws. The proposals relating to the CSRD have been considered by both the European Council and the European Parliament. In December 2025, a provisional agreement was reached between the institutions on the simplification of the CSRD. On 27 February 2026, the revised version of the CSRD was published in the Official Journal. These are amendments to the Directive.

How do the Omnibus proposals amend the previous version of the CSRD?

The Omnibus proposals amend the CSRD in several respects. The main amendments are:

Limitation of scope

In the amended CSRD, the group of undertakings required to report has been reduced. The CSRD now applies to:

EU undertakings with more than 1,000 employees and an annual net turnover of more than €450 million;

non-EU undertakings, provided that the parent undertaking has generated a net turnover of more than €450 million for two consecutive financial years and the subsidiary or branch in the EU has a net turnover of more than €200 million.

Strengthening of the value chain cap

Undertakings that fall within the scope of the CSRD may not request more information from undertakings in their value chain with fewer than 1,000 employees than can be reported under the voluntary standard (VSME). This group is also referred to as ‘protected undertakings’. These undertakings have the right to refuse a request for information if the requested information is not included in the VSME. The undertaking subject to the CSRD is also required to inform protected undertakings of this right when submitting a request that goes beyond this scope.

Simplification of the ESRS

The sustainability reporting standards are simplified, for example through a reduction in reporting requirements and the use of more accessible language.

No sector-specific standards

The obligation for the European Commission to adopt sector-specific standards has been removed. However, the Commission still has the option to develop voluntary sector-specific guidance.

Assurance with limited assurance

The possibility of a future requirement for reasonable assurance on the sustainability report has been removed. Only limited assurance will be required, also in the future. Reference is made to question (What is the role of the accountant in the sustainability report?) for further explanation on assurance.

Transitional provision ‘wave 1’

EU Member States are given the option to exempt undertakings that have been subject to reporting requirements since the 2024 financial year but fall outside the scope of the amended CSRD. This group of ‘wave 1’ undertakings may be exempted from reporting for the financial years 2025 and 2026.

Scope - to whom does the CSRD apply

Who is obliged to report under the CSRD?

The CSRD applies to large public-interest entities for financial years starting on or after 1 January 2024.

Public-interest entities (PIEs) are, amongst others, undertakings listed on an EU/EEA regulated market, banks and insurance undertakings. A large public-interest entity has (on average during the financial year) more than 500 employees and either a balance sheet total of more than €25 million and/or a net turnover of more than €50 million.

From financial 2027 the CSRD applies to:

EU undertakings with more than 1,000 employees and an annual net turnover exceeding €450 million.

From financial year 2028 the CSRD applies to:

Non-EU undertakings, provided that the parent company has generated a net turnover exceeding €450 million for two consecutive financial years and the subsidiary or branch in the EU has a net turnover exceeding €200 million.

Do undertakings outside of the EU have to comply with CSRD requirements?

From financial years starting on or after 1 January 2028, certain subsidiaries and branches in the EU, as well as a parent undertaking outside the EU, will be required to prepare a sustainability report providing insight into the entire undertaking. This obligation applies where the subsidiary or branch in the EU has a net turnover of more than €200 million, and the parent undertaking outside the EU has generated a net turnover of more than €450 million for two consecutive financial years.

Does the CSRD reporting obligation affect undertakings in the value chain, such as suppliers or customers?

Undertakings that do not themselves have a reporting obligation are still expected to experience the effects of the CSRD. Undertakings that are required to report under the CSRD must disclose various material sustainability indicators in their value chain, such as CO₂ emissions. This means that undertakings that, for example, supply to or produce for an undertaking subject to the CSRD, may be requested to share information on various (but not all) sustainability indicators with that undertaking. The maximum amount of information that may be requested is limited to the information included in the VSME.

Does the obligation to prepare a sustainability report apply if I am part of a group?

The principle of annual reporting is that insight is provided into (i) each individual undertaking and (ii) the group of undertakings (consolidation). There are exceptions to this principle. Many undertakings are part of a group. To reduce administrative burdens within a group, it is possible – under certain conditions – for group undertakings to be exempted from the individual reporting obligation. In that case, the sustainability information must be included in the consolidated report of the head of the group (the parent undertaking).

In addition, exempted group undertakings must include a reference in their management report to the consolidated sustainability report – the report of the parent undertaking that also includes the sustainability information of the group undertaking. This exemption is comparable to the exemptions for the financial statements. Users of sustainability information obtain access to the sustainability information and insight into the entire group because the sustainability information is provided by the parent undertaking.

The standards ESRS

What are the European Sustainability Reporting Standards (ESRS)?

The European Sustainability Reporting Standards (ESRS) define the content and structure of the sustainability report under the CSRD. The architecture is similar in each ESRS, as the same reporting areas and topics are required to be reported on.

The ESRS are developed by EFRAG. EFRAG prepares draft ESRS and submits them as advice to the European Commission. The European Commission subsequently adopts the ESRS as directly applicable EU legislation, without the need for transposition into national law. This means that the rules apply directly in all EU Member States.

The standards contain requirements for sustainability reporting, part of which is mandatory for every undertaking. Through a materiality analysis, the undertaking determines which additional sustainability reporting requirements are applicable. This may mean that an undertaking does not report on all data points within a material ESRS standard, as not all elements may be material.

If there are sustainability topics that are material to the undertaking but are not covered by the ESRS, the undertaking must report on these. This is referred to as ‘entity specific’ sustainability reporting.

What do the ESRS-standards look like?

Disclaimer: In the Omnibus proposal, the European Commission has proposed to simplify the reporting standards and requested EFRAG to provide technical advice. In December 2025, EFRAG published revised ESRS. These standards have not yet been adopted by the European Commission through a delegated act. This answer therefore relates to the current ESRS and not to the revised ESRS developed by EFRAG. Please see Chapter 3 for more information on the Omnibus proposals.

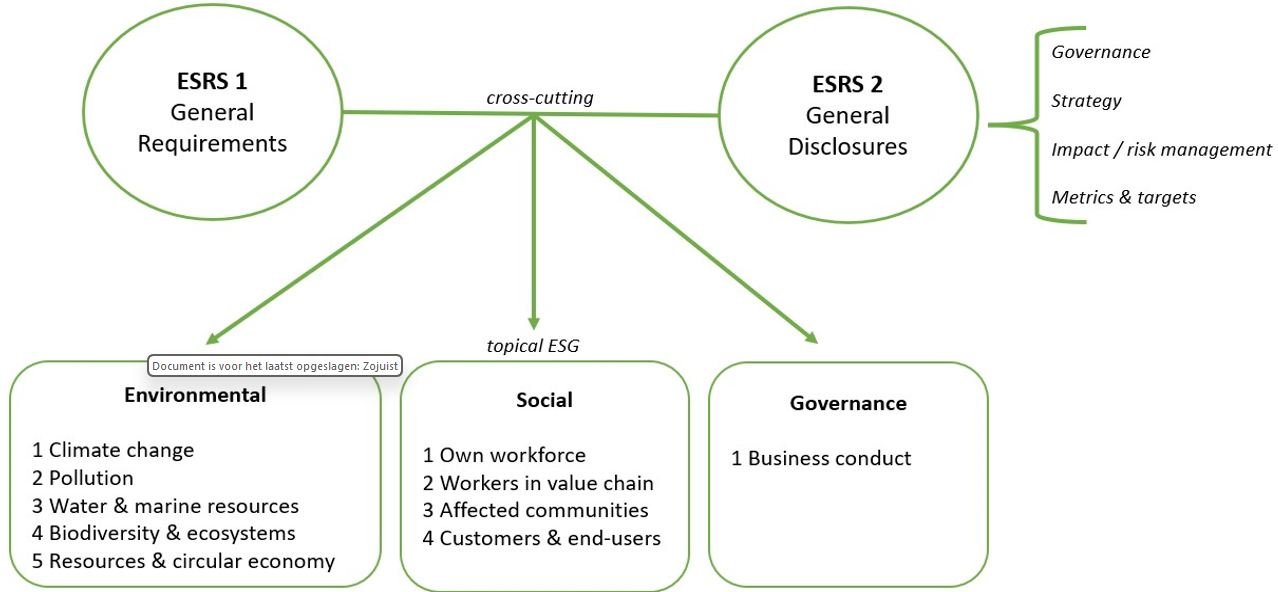

The ESRS consist of twelve standards that apply to all undertakings in all sectors that fall under the CSRD. The twelve ESRS are divided into:

two cross-cutting standards (ESRS 1+2) containing the general requirements and general clarifications, which are necessary for the ‘thematic standards’; and

ten topical standards (E1 to E5, S1 to S4 and G1).

the 'topical' ESRS contain the disclosure requirements for the ESG topics. Within each of the topics there are disclosure requirements for, inter alia, governance (GOV), strategy and business model (SBM), impact-, risk and opportunity management (IRO) and metrics and targets (MT).

See below a schematic representation of these twelve sector agnostic standards divided into two cross-cutting standards and ten thematic ESG standards.

Which cross-cutting standards are there?

There are two cross-cutting ESRS:

ESRS 1 General requirements

ESRS 2 General disclosures

These two ‘cross cuttings’ standards form the basis of the sustainability report and contain the 'playbook' and disclosure requirements for the sustainability report of any undertaking. The thematic E, S and G-ESRS contain references to these cross-cutting standards.

Impact on undertakings that fall outside the scope of the CSRD

What is the impact of the CSRD on undertakings that are not required to report?

Undertakings with fewer than 1,000 employees and a net turnover below €450 million fall outside the scope of the CSRD. They are not required to prepare a sustainability report. However, these undertakings may be indirectly affected by the CSRD.

Undertakings that do fall within the scope of the CSRD are required to report on various indicators within their value chain. As a result, undertakings that are not subject to reporting obligations, but for example act as suppliers or producers for a reporting undertaking, may be requested to provide sustainability information such as CO₂ emissions or may be required to comply with sustainability requirements through contractual arrangements.

Undertakings that are not required to report can also use the CSRD to proactively demonstrate their sustainability activities. They may choose to report voluntarily. By doing so, they can for example support customers by providing insight into their sustainability performance and the information they have available.

For these undertakings, voluntary European sustainability reporting standards have been developed.

What is the VSME reporting standard?

The VSME is a voluntary sustainability reporting standard recommended by the European Commission.

All undertakings that fall outside the scope of the CSRD may be faced with data requests from reporting undertakings within their value chain. The VSME sets a limit on the information that undertakings subject to the CSRD may request from undertakings in their value chain that are not required to report. This is referred to as the ‘value chain cap’.

In addition, undertakings that wish to prepare a sustainability report on a voluntary basis can make use of the VSME standard. The VSME does not require a double materiality analysis and does not require an assurance statement from an external auditor.

The final version of the VSME was submitted by EFRAG to the European Commission in December 2024. On 30 July 2025, the European Commission published a formal recommendation (Recommendation EU 2025/1710) in which it recommends the use of the VSME for micro, small and medium-sized undertakings (SMEs). As part of the Omnibus proposals, the European Commission has indicated that the VSME may be further amended. At present, the recommendation for all undertakings outside the scope of the CSRD is to use the VSME.

The purpose of the VSME is to enable undertakings to report and provide information on:

how the undertaking has had, or is expected to have, a positive or negative impact on people or the environment in the short, medium or long term; and

how environmental and social issues have affected, or are expected to affect, its financial position, performance and cash flows in the short, medium or long term.

The VSME consists of two levels:

the basic module;

the comprehensive module.

When an undertaking reports based on the VSME, it must always report at least on the basic module. An undertaking may choose to supplement this with the more extensive comprehensive module. The comprehensive module builds on the basic module. The basic module is a prerequisite for reporting on the comprehensive module.

Below is an overview of topics and requirements for both the basic and comprehensive modules.

(B) = Basic

(C) = Comprehensive

E - Environment

S- Social

G- Governance

(B) Energy and greenhouse gas emissions

(B) Workforce general characteristics

(B) Convictions and fines for corruption and bribery

(B) Pollution of air, water and soil

(B) Health and Safety -

(C) Revenues from certain sectors and exclusion from EU reference benchmarks

(B) Biodiversity – Biodiversiteit

(B) Remuneration, collective bargaining and training

(C) Gender diversity in the governance body

(B) Water – Water

(C) Human rights policies and processes - and complaints

(B) Recourse use, circular economy and waste management

(C) Severe negative human rights incidents

(C)GHG reduction and climate transition

(C) Climate risk

E - Milieu

(B) Energy and greenhouse gas emissions – Energie en uitstoot van broeikasgassen

(B) Pollution of air, water and soil – Vervuiling van lucht, water en bodem

(B) Biodiversity – Biodiversiteit

(B) Water – Water

(B) Recourse use, circular economy and waste management – Grondstoffengebruik, circulaire economie en afvalbeheer

(C) GHG reduction and climate transition – Reductie van broeikasgassen en klimaattransitie

(C) Climate risk – Fysieke risico’s door klimaatverandering

S - Sociaal

(B) Workforce general characteristics – Algemene kenmerken van het personeelsbestand

(B) Health and Safety - gezondheid en veiligheid

(B) Remuneration, collective bargaining and training - beloning, collectieve onderhandelingen en opleiding

(C) Human rights policies and processes - and complaints – Impact op mensenrechten en klachten

(C) Severe negative human rights incidents – Ernstige negatieve mensen rechten schending

G - Governance

(B) Convictions and fines for corruption and bribery - Veroordelingen en boetes wegens corruptie en omkoping

(C) Revenues from certain sectors and exclusion from EU reference benchmarks - Inkomsten uit bepaalde sectoren en uitsluiting van EU-referentiebenchmarks

(C) Gender diversity in the governance body - Genderdiversiteit in het bestuursorgaan

Practical implementation and enforcement

How should the information be reported?

The sustainability report is part of the management report. The sustainability report should be a recognizable section of the management report. In the Netherlands, the management report, containing the sustainability report, must be submitted each year to the Chamber of Commerce (‘KvK’) and will probably be required to be available online. Whether this is indeed required will follow from the definitive implementation of the CSRD in Dutch law. Undertakings are obliged to provide information in a digital format and deposit the sustainability report in XBRL format whereby the information contained therein should be tagged. Tagging means the digitally marking of data. This allows data to be processed automatically. XBRL (eXtensible Business Reporting Language) is an open standard that facilitates this tagging. The classification system of the European Sustainability Reporting Standards set 1, also called ESRS XBRL Taxonomy, defines which data should be tagged. In August 2024, EFRAG's proposed ESRS XBRL taxonomy has been handed over to the European Commission and the European Securities and Market Authority (ESMA). For more information, see the EFRAG XBRL Taxonomy webpage.

A central European Single Access Point (ESAP) is currently being developed. The aim is that stakeholders will be able to electronically access all public financial and sustainability information of undertakings in Europe via this ESAP. The regulation has been in force since January 2024 and aims to be operational by 10 July 2027. This digital platform, developed by ESMA, will gradually centralise financial and sustainability data of EU undertakings, starting in July 2026.

Does the sustainability report have to be audited by an external auditor?

The sustainability report must be assessed by an external auditor. This may be the external auditor that also audits the financial statements but may also be another external accountant. In the Netherlands, other ‘assurance providers’ other than an external accountant may not assess the sustainability report.

The minimum requirement for external assessment of the sustainability report ('limited assurance') under the CSRD is less thorough than an external audit of the financial statements ('reasonable assurance'). However, the required assessment of the sustainability report does go considerably beyond the effort currently required and conducted by an external auditor to assess the management report. An example of what the external assurance provider is looking for is in the selection of stakeholders as part of the materiality analysis. A way in which an external assurance provider executes assurance procedures would be to look into the value chain of the undertaking and see if important stakeholders in this process are included in the materiality analysis. Through this, they see if an undertaking’s stakeholders who may be directly or indirectly impacted by the activities of the undertaking play a role in the analysis.

For the external assessment of the sustainability report, the external auditor provider shall perform an audit of all required information presented in the sustainability report and whether it corresponds to the undertaking’s actual sustainability performance and the completeness thereof. The external auditor will only provide a limited content-related assessment on what is reported.

Who can provide an assurance opinion on the CSRD-related sustainability reporting?

The CSRD outlines 3 member state options for assurance provision:

the statutory auditor who audits the financial statements;

another external auditor or accountant who does not perform the financial audit;

an independent assurance provider as designated by the member state. As this is a Member state option, it is not clear if this will be permitted under Dutch law.

In the Netherlands, other 'assurance providers' are not allowed to issue an assurance statement in relation to the sustainability report.

How can an undertaking prepare for auditor assurance on the sustainability report?

It recommended to involve the auditor in the preparations for the annual report as early as possible at the beginning of the CSRD preparation process. It is beneficial to go through the structure of the assurance work with the auditor and the undertaking at an early stage. In this way, clear arrangements can be made about the nature and timing of the work of the accountant and the desired audit trail (recording of the documentation needed to test the reliability of the sustainability information in the annual report).

It is also desirable if the auditor carries out an early review of the materiality analysis process and the related selected sustainability topics that can be reported on. After all, if the auditor concludes later in the process that another sustainability topic should also be reported on, it is difficult or impossible for the undertaking to include that information in the annual report as well. It is therefore a good idea to have the auditor review the selection of topics and the associated materiality process shortly after completion of the materiality analysis, or already before or during the process.

The Royal Netherlands Institute of Chartered Accountants also recommends starting the process at an early stage.

What if you do not or do not fully comply with the CSRD and the ESRS?

An undertaking complies with the disclosure requirements where the undertaking discloses all material information in a timely manner and in the ESRS described manner. Even if the undertaking is not (fully) sustainable, the undertaking can still comply with the CSRD and ESRS when the sustainability report accurately reflects how sustainable the undertaking is. The ESRS encourage undertakings to provide the timeframe in relation to providing insight in the missing information.

An undertaking does not fully comply with the CSRD and the ESRS when material information is missing from the sustainability report. The auditor will report this in his statement. Failure to file the sustainability report or not filing it in time, is an economic offence.

What are the effects of the CSRD on annual reporting?

By making a sustainability report mandatory, the content of the management report will expand significantly. Undertakings subject to reporting requirements shall have to report the material sustainability information in their management report.

The sustainability information may have no direct impact on the financial statements, however, it is to be expected that (internal and external) developments in the area of sustainability can have an impact on the financial statements (e.g., the shortening of the remaining service life of machines that will be replaced earlier than expected by more sustainable machines).

What is the effect of in the CSRD on the value chain?

The effect of the CSRD on the value chain is that value chain partners of reporting undertakings, including those that are not required to report, may receive information requests. The CSRD and ESRS require undertakings to disclose sustainability information from their value chain. Undertakings therefore need insight into their value chain, for example knowledge of how purchased products are produced and what happens to them after sale. Please see Chapter 6 (Impact on undertakings that fall outside the scope of the CSRD).

There are specific ESRS-standards, such as ESRS S2 and ESRS E1 which require value chain information, including health and safety of employees in the value chain and CO2 emissions. You need your value chain partners to report in accordance with the CSRD. For more information, reference is made to EFRAG's implementation guideline on the value chain. Expected revisions to the ESRS will lead to the development of new guidance supporting data requests.

Are undertakings within a group, including parent or subsidiary undertakings, considered part of the value chain?

Normally, the sustainability reporting is drafted by at the parent undertaking level in one consolidated report. In this consolidated sustainability report, all subsidiaries are included as part of its own operations. The value chain refers primarily to business partners, such as suppliers and customers, that are not part of the undertaking.

If for example a European undertaking drafts a report, but has an American parent undertaking (with no CSRD reporting obligations), this American parent undertaking might be considered part of the value chain depending on the value chain relationship it has with the European undertaking /subsidiary.

What should be done if value chain partners cannot provide the necessary sustainability information supply?

Obtaining sustainability information from the value chain is more difficult than obtaining information from one's own undertaking. The CSRD takes this into account by allowing the use of estimates and assumptions when primary supply-chain information is unavailable. Consider estimates, sector averages, or other indirection information sources. The undertaking should clearly identify what estimates and assumptions have been used in the preparation of the sustainability information and what measures have been taken to ensure accuracy.

What is the role of an IT system?

An IT system supports the collection, integration and reporting of detailed data from various sources for the sustainability report. It improves data management processes and supports digital preparation and submission of the sustainability report. Software providers are expected to develop tools for tagging, data integration via APIs and automatic structuring of data in the CSRD format, including notifications for missing information.

Where should the sustainability report be filed?

The implementation of the CSRD is still ongoing. There is currently no formal filing obligation for the sustainability report.

The management report, including the sustainability report, must be filed annually with the trade register of the Dutch Chamber of Commerce (in Dutch: KvK), and will likely also need to be published on the undertaking’s website. Listed undertakings must file the sustainability report with the Authority for the Financial Markets (AFM). The AFM will only formally supervise once the CSRD has been implemented in Dutch law.

Where can I find examples of undertakings required to report under the CSRD?

We would like to refer you to the following information in which you can see examples of undertakings already reporting under the CSRD. In doing so, we are not passing a value judgment on the examples in question, but rather aim to provide a picture of what is happening in the field. Examples:

AFM report ‘No time to lose’

- See in particular the 'Good Practices'

How can an undertaking prepare for the approaching sustainability reporting obligations?

Sustainability reporting may be relatively new for many undertakings, and the sustainability report will become a comprehensive part of the management report. In short, it is a challenge and it takes time to get it (right). And therefore, the key advice is: start and start now. But not everything has to be done at once.

For example, one could start as follows:

Map out how your undertaking affects the environment and how the environment has an impact on the undertaking. To understand this, it is necessary that to have insight into where, what, and how the undertaking purchases and sells goods or services.

Identify which people within your undertaking are involved with (aspects of) sustainability.

Map blind spots: what do you already know (and/or measure) in the field of ESG and what topics are new to you? Who is responsible in your organization for these topics?

Learn from others. Look into ESG reports from undertakings in your industry that are already reporting on sustainability. What do they publish?

Discuss it with an advisor, or your accountant.

Join existing initiatives where undertakings can get practical tools. The sector covenants for IRBC, for example, developed various instruments and tools (in Dutch) with many examples on how undertakings are reporting. See also the SER-website (in Dutch) on the due diligence guidelines. But also, organizations such as UN Global Compact, Future Up (former MVO Nederland) or your industry association can help you further.

Reporting on sustainability indicators often requires a thorough system to collect information. Which information systems are already available within the undertaking and do these meet your reporting requirements? And what information is needed from value chain parties? It is also important to inform those parties about the impending reporting obligation.

Voluntary reporting based on the VSME provides a low-threshold starting point for sustainability reporting for undertakings that are not, or not yet, subject to the CSRD and ESRS.

What are possible challenges for undertakings in the upcoming mandatory sustainability report?

The lack of a solid IT system complicates the reporting process and makes reporting labour intensive. For the sustainability report, reliable sustainability data is needed. Good IT systems to improve filing the sustainability data of one's own organization and value chain information (upstream and downstream) will be helpful.

The lack of knowledge about the value chain can be a challenge as well. Undertakings need insight into the products or services they purchase, where and how their product or service is created and what happens after they sell the product or service. That means that information is needed, also from value chain parties with whom no business is done directly. It is important to perform a good materiality analysis, because this analysis determines what you need to report on.

Simultaneously becoming more sustainable and reporting on sustainability can be a challenge. The new sustainability reporting obligation may lead to a desire to become more sustainable (faster). To make sustainable improvements, and deliver a good sustainability report, sufficient attention and time within the entire organization as well as buy-in from top management is needed.

How can an undertaking start to fulfil the obligations arising from the CSRD and ESRS?

Ensure that top management has knowledge about the CSRD and recognizes the importance of the CSRD.

Read the CSRD, ESRS, and VSME. Find useful links below for more information.

Identify which departments and individuals within your organisation are already collecting information on the requested data points.

Map out where there is insufficient knowledge within the organization and make sure that the knowledge is increased or obtained.

Connect your value chain partners as soon as possible, so that you can prepare together. For instance, think together about strategy, making impact and being able to ensure that the correct data can be shared in the context of data requests related to the CSRD. It takes time to set this in motion and being able to collect the data. If you start working on your own first then you miss an opportunity to work with your chain as a joint effort.

What are useful links with more information about the CSRD/ESRS?

University of Groningen Business School (UGBS) essay series ‘Sustainability Reporting after the CSRD (in Dutch: ‘Duurzaamheidsverslaggeving na de CSRD’ (available in Dutch only)

How can I easily explain internally how to get started?

The Research Centre for Sustainable Organisations has put together an illustration (in Dutch only) with the help of experts within the fields of business models, labour, employment, HR, impact marketing, partnerships and financing, integrated reporting and impact measurement to inspire undertakings to get started.

Source: Research Centre For Sustainable Organizations HOGENT

What role can my industry association play with respect to the CSRD?

Industry associations can play an important role in supporting undertakings in preparing for CSRD reporting, as many impacts, risks and opportunities are sector-specific. Contact your industry association to find out how they can support you.

Examples of the role of an industry association could play are:

Facilitate a sector-specific process on identifying material impacts, risks and opportunities for a sector:

Perform sector-specific risk analysis - providing insight into risks likely to occur in the sector as a resource for members

Provide aggregated data sets, based on the data of the undertakings in the industry

Identify stakeholders and weigh their interests;

Bring together joint stakeholders, such as NGOs, banks, trade unions, consumer organisations, so that they can provide input for the materiality analysis;

Help prepare questionnaires for materiality analysis;

Collect and share good examples from undertakings within a sector.

Improve insight in the industry on ESG themes:

Information campaigns targeting functions within the undertakings such as senior management, supply chain, purchasing, compliance, finance and HR;

Offer tools to strengthen this process;

Identify connections with other legislation.

Provide feedback on the development of the ESRS through public consultations and participation in expert working groups at EFRAG.

Undertakings are responsible for their own reporting, but working with an industry association can provide insight into the common process and how others deal with it. There will be a undertaking-specific difference due to different choices and financial possibilities.

Relationship with existing national and EU legislation and other standards

How does the CSRD relate to existing and future sustainability legislation?

The CSRD is one of the initiatives that fits within the European “Green Deal” and other national and international legislation and regulations in the field of International Responsible Business Conduct (IRBC) and sustainability.

Dutch guidelines

Dutch Corporate Governance Code, and other laws and regulations that regulate the substance to the management report

The CSRD/ESRS is an addition to the current rules for the management report. Information that is already part of the management report based on existing laws and regulations will continue to be included. It is intended for the ESRS to allow cross-references to avoid duplication. The exact interpretation of this is still unclear.

European legislation, directives and agreements

European sustainability legislation, objectives and directives mainly originate from the EU Green Deal. The EU Green Deal was introduced in 2019 as a response to the Paris Climate Agreement of 2015.

Topics for which policy has been developed under the EU Green Deal:

Source: Europe’s European Green Deal: mobilising industry, preserving biodiversity, supplying clean energy, smart mobility, and more (European Commission publication, 2020)

Below you can find an overview of several European regulations and directives that, like the CSRD, form part of the EU Green Deal and relate directly or indirectly to the CSRD.

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD establishes a corporate due diligence obligation for large companies to identify and address adverse human rights impacts (such as child labour) and environmental impacts (such as pollution) in their own operations, those of their subsidiaries and in their “chain(s) of activities”. The CSDDD, like the CSRD, was part of Omnibus I and has been amended in certain respects. See the revised version of the CSDDD.

The CSDDD refers to existing legislation for certain obligations. For example, regarding public communication on due diligence, the directive relies on reporting under the CSRD, thereby avoiding duplication for companies within the scope of both frameworks.

EU Taxonomy

The EU Taxonomy is a classification system that defines which economic activities can be considered environmentally sustainable. Undertakings within the scope of the CSRD must also report on how and to what extent their activities are aligned with the EU Taxonomy. Although both the EU Taxonomy and the CSRD address the same environmental topics, they take different approaches, resulting in different reporting requirements. The EU Taxonomy was also part of Omnibus I and has been amended. See the revised version of the EU Taxonomy.

Sustainable Finance Disclosure Regulation (SFDR)

Financial market participants subject to the SFDR require sustainability data from the undertakings in which they invest. These undertakings are required to report under the CSRD, and the sustainability report provides the information needed under the SFDR.

Forced Labour Regulation

This regulation prohibits the placing of products made with forced labour on the European internal market. It assigns enforcement responsibility to national authorities based on a risk-based approach. The CSRD requires undertakings to report on labour relations, including forced labour, under ESRS S2.

Regulation on Deforestation-free products

This regulation prohibits the placing or making available of products that contribute to deforestation and forest degradation within the European internal market. It requires insight into the value chain of products. Like the CSRD, this regulation is part of the European Green Deal. Reporting on ecosystems and biodiversity may form part of the sustainability report, see ESRS E4.

International guidelines and agreements

Paris Climate Agreement

The climate agreement is an international treaty signed by nearly 200 countries to limit global warming. The European Union has committed to this agreement, and the CSRD is a concrete way for the EU to implement it.

OECD Guidelines for Multinational Enterprises (OECD MNE Guideline)

These are international standards for responsible business conduct. The guidelines provide tools for undertakings to address issues such as value chain responsibility, human rights, child labour, environment and corruption. The CSRD and the ESRS explicitly refer to these guidelines in several places, for example requiring that the assessment of negative impacts is guided by the due diligence process as set out in the OECD guidelines.

United Nations Sustainable Development Goals (SDGs)

The Sustainable Development Goals for 2030 are seventeen goals aimed at making the world a better place. The CSRD can be seen as a practical implementation of the SDGs, using transparency to contribute to sustainable development from a European perspective.

United Nations Guiding Principles on Business and Human Rights (UNGPs)

These are international standards for responsible business conduct. The CSRD and the ESRS explicitly refer to these principles in several places.

International sustainability reporting standards

Standards of the International Sustainability Standards Board (ISSB)

The ISSB is a sister organisation of the IASB (developer of IFRS: International Financial Reporting Standards). The ISSB has developed international sustainability standards, the IFRS Sustainability Standards (IFRS-S). The European Commission and EFRAG have sought alignment with these standards where possible, in order to reduce reporting burdens for undertakings applying both CSRD/ESRS and IFRS-S. See the ‘ESRS-ISSB Standards Interoperability Guidance’ published by EFRAG and the IFRS Foundation for more information.

Global Reporting Initiative (GRI)

The GRI is an international standard setter that develops and maintains sustainability reporting standards. The GRI standards are widely used globally and focus on reporting the material impacts of an organisation on the economy, environment and society (impact materiality). Unlike the ISSB standards, which focus primarily on financial materiality for investors, GRI applies a broader stakeholder approach. In developing the ESRS, alignment with existing GRI standards has been sought. EFRAG and GRI have also entered into cooperation agreements to increase interoperability and reduce unnecessary reporting burdens.

Corporate initiatives

Science Based Targets

Science Based Targets are CO2 reduction targets that have been assessed as in line with keeping global warming to 1.5 degrees. The ESRS (Climate standard (E1)) also uses 1.5 degrees as a reference point. For example, the undertaking must report whether the CO2-reduction plans are in line with the 1.5-degree scenario. The institution that can assess undertaking’s plans on this 1.5-degree objective is the Science Based Target initiative (SBTi) - a collaboration between four non-governmental organizations (NGOs), UN Global Compact, the Carbon Disclosure Project (CDP), World Wildlife Fund (WWF) and the World Resource Institute (WRI). Undertakings are not obliged by the CSRD to set targets that are in line with Science Based Targets.

Which other CSRD-related legislation (related to the CSRD) plays a role in the work of the SER?

The SER is involved in various topics and national legislation that are closely related to social factors to be reported on under the CSRD. Below are some examples that can help undertakings to achieve meaningful reporting:

Occupational Safety and Health Platform (OSH Platform)

(Dutch Occupational Health and Safety Act): The OSH Platform is the central information point of social partners on healthy and safe working. The OSH Platform offers advice, knowledge exchange and inspiring examples to employers, employees and health and safety experts. Moreover, people can ask questions. The aim is to work together on good working conditions.

Diversity (e.g. legislation on diversity at the top):

for large companies in the Netherlands, since 1 January 2022, a legislation on diversity at the top (in Dutch: Wet ingroeiquotum en streefcijfers) applies, which aims to make the ratio of women to men in the top and sub-top more balanced. Large companies must report to the SER on the male-female ratio in the management board, supervisory board (rvc) and sub-top. They must also show what targets and corresponding plans of action they have drawn up to increase diversity in the (sub)top. The SER Data Explorer shows the information from the annual reports of these large companies and makes visible the information and development of gender balance in business;

in addition, SER Top Women makes highly qualified boardroom-ready women in the Netherlands visible by including women with talent and ambition in the database of SER top women. This aims to boost the advancement of women to top (sub)top positions;

SER’s division ‘Diversity within Companies’ (in Dutch: Diversiteit in Bedrijf also supports organisations in promoting a mixed workforce and an inclusive business climate. SER Diversity within Companies focuses on five dimensions: work ability, cultural diversity, gender, age and LGBT+, including in the form of the Diversity Charter.

Co-determination (Dutch Works Councils Act):

The SER's co-determination knowledge centre advises works councils, directors and supervisors on current, social-economic developments that influence co-determination. In doing so, the SER aims to promote the proper functioning of organisations.

For more information on the (possible role) of a works council in relation to sustainability in general, please see this website of trade union FNV.

International responsible business conduct:

The SER plays an important role in the creation and implementation of IRBC agreements. An IRBC agreement is a cooperation in a sector between companies, the government, trade unions and civil society organisations. They make agreements in the covenants to tackle and prevent abuses such as exploitation, animal suffering or environmental damage. The SER runs the secretariat of most IRBC agreements.

Role of different parties involved in the creation of the ESRS

What is the role of the European Commission and EFRAG in relation to the CSRD?

The European Commission is responsible for the creation of the ESRS. However, the European Commission makes use of EFRAG’s technical advice. For example, EFRAG drafted Set 1 of ESRS and submitted this to the European Commission in November 2022 (as an advice). This was followed by the European legislative process. The European Commission is obliged to request advice from European authorities, such as ESMA, EBA and EIOPA, on EFRAG’s proposal. The European Commission may review the opinion of EFRAG (and content of the ESRS).

What is EFRAG and which parties participate in it?

EFRAG previously was the abbreviation for the European Financial Reporting Advisory Group and is a collaboration between various national and European stakeholders on reporting. Originally EFRAG only advised the European Commission on financial reporting, such as the implementation of IFRS. EFRAG also develops reporting standards for sustainability reporting, the ESRS. The stakeholders of EFRAG include national standard setters for financial reporting, and European bodies such as for example Business Europe, Accountancy Europe and the European Federation of Financial Analysts Societies (EFFAS). In addition, European authorities such as ESMA, ECB etc. are involved. For sustainability reporting, there are also specific numbers of other parties affiliated with EFRAG such as NGOs, trade unions, consumer organisations and academics.

How is the DASB involved in EFRAG regarding sustainability?

The DASB participates (as the Dutch reporting standards setter) in EFRAG and is also a member of (the boards of) both the financial reporting pillar as well as the sustainability reporting pillar of EFRAG. The DASB has a dedicated sustainability working group that supports it on matters relating to sustainability, including reviewing and providing comments on EFRAG’s (and ISSB) standards process, which enables the DASB to respond appropriately within EFRAG (and ISSB).

Additionally some DASB representatives are appointed members of different EFRAG governance bodies. Also some members of the DASB sustainability working group are appointed as member of the EFRAG Sustainability Reporting Board (SRB) and EFRAG sustainability working groups.

EFRAG SRB is responsible for providing the definitive technical advice (the ESRS) of EFRAG to the European Commission.

How is the SER involved in EFRAG regarding sustainability?

The SER is not directly involved in EFRAG. However some SER employees were involved in a personal capacity with EFRAG in the 'Sustainability Reporting Technical Expert Group' (EFRAG SR TEG), the 'social expert working group', the 'SME expert group' and the 'implementation guidance value chain working group'. The SR TEG supports the SRB. In addition, several employees of the SER are members of the RJ sustainability working group.

Latest updates

On 3 July 2026, the European Commission adopted delegated acts for the simplified ESRS and the voluntary standard. The delegated act revising the ESRS and the delegated act establishing the voluntary reporting standard will now be submitted to the European Parliament and the Council of the European Union for scrutiny. The standards will enter into force once the two month scrutiny period has expired. This period may be extended by another two months.

The CSRD has undergone several changes as a result of the Omnibus proposals. What the Omnibus entails and which changes have been implemented can be found in Chapter 'Amendments to the CSRD through the Omnibus proposals' of the CSRD, ESRS and VSME frequently asked questions and answers. On 27 February 2026, the revised version of the CSRD was published in the Official Journal. Based on this new version, the frequently asked questions and answers have been updated. In addition, the implementation of the CSRD into Dutch legislation has not yet been completed. Once these developments are finalised, the frequently asked questions and answers will be updated accordingly.

Questions CSRD & ESRS

Do you have questions about the CSRD, ESRS or are you missing a question in this list? Send us an e-mail and we will contact you as soon as possible.

Questions regarding individual facts or circumstances will not be answered through these channels. For such questions, we recommend that you contact an advisor such as your company accountant.

Disclaimer

The SER and the DASB have put this questions and answers document together based on publicly available information at the time of publication. Although these questions have been answered with the utmost care, users of this document cannot be given any guarantees relating to the accuracy, topicality and completeness of the information displayed. The SER, the DASB and other parties related to this document cannot be held liable for the consequences of the use of the information from this document. This document does not represent the view of (EFRAG) or the European Commission, nor the SER or DASB.

It is not permitted to copy or distribute the included information or individual elements (including images) without explicit permission, if this may cause confusion about the origin of the material.

Download Questions and answers

Read the frequently asked questions and answers about the CSRD.